Which is the Best Payment Gateway in the UAE for my E-Commerce Store?

More Blogs

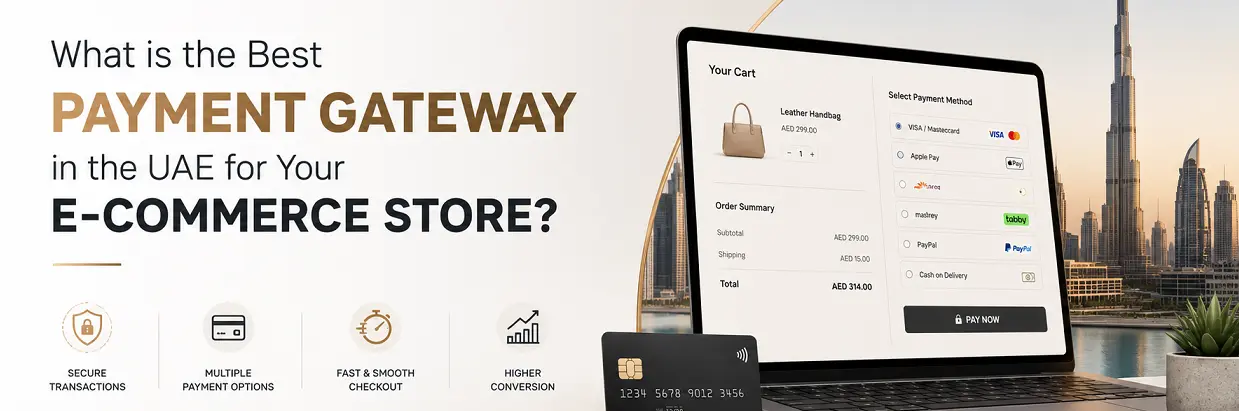

If you’re building an online shop in Dubai, Abu Dhabi, or across the Emirates, there’s this one question that pops up right away: “How do I accept payments securely from my customers without getting eaten up by hidden fees?”

With the UAE retail space growing fast, choosing the right payment setup is one of those decisions that can really shape your results. A checkout that feels clunky, or an integration that keeps acting unpredictable, doesn’t just irritate people, It straight up lowers your conversion rates. And if your site sends shoppers through weird steps, like unnecessary redirects, or it doesn’t properly support localized digital wallets such as Apple Pay, those customers will often just leave the tab and go buy from someone else.

To make it easier, this guide walks through how payment systems work “under the hood”, lists the top three payment gateway options showing up across the UAE market, and explains how to pick what fits your business setup, not just what sounds good on paper.

How online payments work?

Before comparing providers, you kind of need the basic map. What actually happens when someone clicks “Checkout” is a chain of events, supported by several layers, all meant to move value safely from the buyer to you.

- The Payment Gateway: This is the piece users indirectly experience. Think of it like a digital terminal that securely captures card details , then tokenizes sensitive data, and runs early checks for fraud signals before it forwards the transaction data onward.

- The Payment Processor: This part works in the background & does the heavy lifting. It routes the transaction through card networks (Visa, Mastercard, or other local channels) to confirm whether the buyer has the available funds, and then continues the flow to approval or denial.

- The Merchant Account / Acquiring Bank: After the transaction is formally approved, the processor works with the financial institutions, so the money lands safely in your business bank account, safe and secure.

When you’re building an online platform, stitching these layers together is not a casual task, it takes specialized technical know-how. Partnering with a professional ecommerce development agency helps your gateway connect smoothly through clean APIs, it also helps you keep PCI-DSS security compliance steady, while the checkout page stays snappy & fast, like it should be.

Top 3 payment gateways in the UAE

Different businesses run on different habits. A small home startup often wants quick onboarding and zero fixed costs , but an enterprise moving through millions of transactions every month usually asks for volume pricing and dedicated account management.

Have a quick look at the top three payment gateway providers in the UAE:

1. Stripe (UAE): Stripe basically has become a kind of gold standard for tech startups, modern SaaS companies, and scaling online retailers across the Emirates. It’s known worldwide for a developer-first setup, and they also launched local operations in the UAE to give businesses another path besides older, slower banking frameworks.

- Fee Structure: It’s completely transparent. You pay 2.9% + AED 1.10 per successful domestic card transaction (actual rates might vary). No setup fees, no ongoing monthly maintenance commitments, and no surprise cancellation penalties are offered by Stripe (conditions might differ).

- The Standout Features: Stripe has a moder polished dashboard, and the API docs are on of the best on the market. It comes with built-in fraud prevention (Stripe Radar) and it supports these clean one-click checkout flows through Stripe Elements. Also it accepts Apple Pay and Google Pay natively right out the gate, which is huge , because mobile wallets are such a big chunk of UAE online sales.

- The Limitations: Their transaction fees can be a bit higher for small-ticket stuff compared to a few local options. Plus customer support is mostly digital only , so you can’t just pop into a local brick and mortar office if something weird happens, like an unexpected account hold.

- Best For: Fast-growing direct-to-consumer (D2C) brands, subscription businesses, and teams running custom web builds that require a flawless mobile customer journey.

2. Network International: Since they’re a locally public-listed enterprise & also the largest payment processor across the Middle East and Africa (MEA) region, Network International is a heavyweight in institutional finance. Their N-Genius platform gives you enterprise-grade infrastructure that’s tightly connected to local banking rails.

- Fee Structure: It’s bespoke, and heavily negotiated based on volume. They may charge upfront activation fees and fixed monthly system charges, but the per-transaction commission rates are often very competitive, sometimes dropping between 1.5% and 2.5% for high-volume corporate accounts.

- The Standout Features: Because N-Genius runs on local banking rails, it offers stable transaction routing for large financial sums, way more solid than many setups. They also provide 24/7 dedicated local account managers , plus phone support. On top of that , they offer direct integrations with regional government payment systems and a pretty full set of social commerce tools (like making secure payment links for WhatsApp & Instagram sales).

- The Limitations: The onboarding process could be time consuming. Plan on waiting 1 to 2 weeks for the compliance checks and for account approval. Their developer APIs , plus the dashboard look and feel, also trail a little behind the slicker international competitors.

- Best For: High-volume enterprises, established brick and mortar retail groups moving online, B2B wholesale merchants, and hospitality businesses that deal with heavy monthly volumes.

3. Tap Payments: Tap Payments is a regional fintech powerhouse built to tackle the particular cross-border problems of the Gulf Cooperation Council (GCC) market. It kind of acts as the bridge between global standards, and local Gulf payment habits.

- Fee Structure: The pricing is highly competitive for regional trade, starting around 2.75% + AED 1 per domestic card transaction, with zero setup fees and no recurring monthly operational charges (actual rates may vary).

- The Standout Features: Tap’s biggest edge is its native regional payment flexibility. While many global gateways handle standard credit cards, Tap lets your store accept local debit networks across the Gulf directly, such as mada (Saudi Arabia), KNET (Kuwait), and Benefit (Bahrain) as well as standard Visa, Mastercard, and Apple Pay. They also mention a very fast digital onboarding flow, often approving compliant accounts within 48 to 72 hours.

- The Limitations: Their analytical reporting tools and developer documentation are functional but lack the extreme depth and custom coding flexibility found in global platforms like Stripe.

- Best For: UAE based e-commerce storefronts where the main expansion move is selling smoothly to people in Saudi Arabia, Kuwait, and the broader GCC area.

Conclusion

Picking a provider is only half of it, because how that provider ends up inside your store code is what decides your profit margins. Clunky plug and play add-ons often bring layout shifts, or cause slow page loads, and sometimes they just can’t manage currency exchanges cleanly, and then you lose folks right away at the moment the customer finally gets to their wallet out.

To push your revenue up, your payment pipeline needs to load in milliseconds and stay fully inside your domain, no disruptive third party redirects. When you combine well targeted payment settings with a high performance custom web development framework, you make sure your database handles user sessions securely, processes tokens the right way, and keeps the checkout funnel annoyingly friction free.

Yes, Buy Now Pay Later services like tabby and tamara are included with top-tier payment gateway providers. BNPL increases the sales as buyers can split their spend to easy installments.

Payout schedule depends on the payment gateway service provider. Usually payment gateways follow a rolling 7-day schedule.

No, payment gateway service providers follow strict checks and validation of your business entity before onboarding. Having a trade license in the UAE is a mandate for requesting payment gateway services.

CLOUD6 is a top ecommerce development agency in Dubai. We offer integrations with all the major payment gateway services providers including BNPL service providers like tabby and tamara.

Payment gateway integration charges depends upon the ecommerce tech stack you are currently having and the API documentation from payment gateway provider. Payment gateway integration for a Shopify site would be in the range of AED 1,500 to AED 2,000 where as custom ecommerce in Php or Python would cost above AED 2,000.